This is a calculator based on relatively simple acturial maths. Its not rocket science. The core reason I have produced this is twofold. In part because in my particular case it was me losing out and, much more importantly the advice given to me by my lawyer (who categorically states this is the position of all lawers and is established practice) is fundamentally and moraly wrong.

“Just because everyone does it does not make it right. Just becuase nobody does it does not make it wrong.”

The core element of this error is assumption. When looking at pre-marital assets, which I agree is a fundamental principle of fairness, lawyers take a straight line approach; assuming the figures will pretty much match up. They are wrong, and quite spectacualrly so. Becuase most people are mathmatically weak; our education system seems to pride itself on leaving people vulnerable when it comes down to money, even my own, highly educated, lawyer took some convincing as to the reality of this error.

The issue is wrappered around compound interest and growth.

What this shows is that your lawyer will only ever get their straight line calculation correct once; that is if the pension was started after marriage.

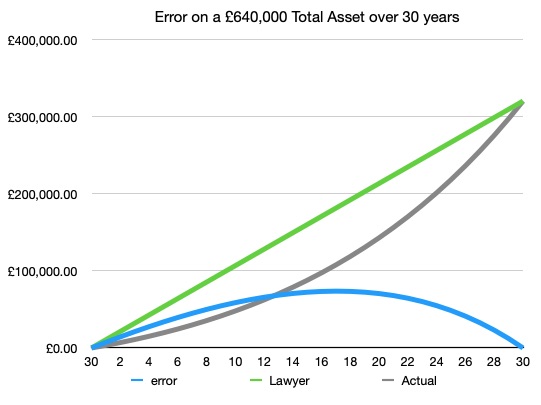

The way to look at this is by taking 30 as the date of separation. In this case the total CETV for the pension is £640,000, and so if the marriage date was at 0 or before the split agreed both acturially correct and agreed by you lawyer will be £320,000. However if the marriage date is inbetween 0 and 30 there needs to be a valuation of the pre-marital asset, and this is where it goes very wrong.

As you can see there is a sweet spot of horror. The figures below are the values split so real money after division.

If, for example, you got married at year 1 your lawyer will say the PMA split is £10,666, where it is actually £3,354. Because this is taken off the total asset the error is c 2%; but still wrong. The worst case is at 17 years where the lawyers PMA split is £181,333 where the real value is £107,711, a 35% error but denies you nearly £75,000. Even if you look at year 29 the lawers PMA split is £309,333 where the real split is £297,141, a 53% error losing you £12,191.

All I can say is lawyers need to take a long hard look at their lack of ability to understand maths.

Try the calculator below to see what difference it makes to your outcomes.

Instructions for use:

Most importantly this is only for situations where the pension was started BEFORE the marriage. It is for working out the correct pension value at marriage and thus the PMA (Pre Marital Asset) and thence the Asset value to be used in the Assets/Liabilities seperation calculations.

I have tried to keep things as simple as possible and it is oddly, given my rants, still skewed in favour of the pension holder, in that it makes some assumptions.

So for example the form assumes a linear career progession with fixed annual pay rises, whereas it is far more likely that there will have been significant jumps in salary. Also I have set the default to 6% which is representitive of a career professional, you may want or need to drop this to better represent you or your partner.

I have set the pension growth to 5% which I believe to be fairly typical. If you know this to be different so adjust accordingly.

The critical field for getting this right is the Contributions field. This may look quite large, but remember this will include employer contributions too. You will need to adjust this number until the Calculated Valuation matches as close as possible the PETV/CETV figure entered. I’ve set a GOOD/BAD flag field at a 0.003% deviation which I guess is close enough.

Good Luck